Wheat Market Update - 31st January 2025

Welcome to this week’s market update! Each week, we'll delve into the market movements and key factors affecting wheat prices. Whether you're a fellow industry professional, a supplier, or simply interested in what’s happening in the market, our updates will offer valuable insights to keep you ahead of the curve.

Market Report

Global Market

Despite the lack of news around tariffs since Trump came into office, they were thrust back into the limelight last week, with Trump threatening tariffs on Columbia if they did not agree to let US planes land with detained illegal immigrants. Over the weekend, it was confirmed that Canada and Mexico would receive at 25% tariff, with China receiving an additional 10% tariff on their goods.

These tariffs could affect global grain prices in several ways. The US, a major grain exporter, may face retaliatory tariffs, reducing demand from key buyers like China and the EU. This could lead to a surplus in the US, driving domestic prices down, while global prices may rise as countries seek alternative suppliers.

Tariffs on imported grains or farming inputs (e.g., fertilisers) could increase US production costs, making grain more expensive. Countries reliant on US grain may also face higher costs. Trade flows could shift, with buyers turning to Brazil, Argentina, or Australia, increasing demand and potentially raising global prices.

Tariff announcements would likely cause market volatility, as traders speculate on supply disruptions. Futures markets may see sharp price swings, driven by policy uncertainty. In the long term, US farmers could cut back production if tariffs reduce profitability, leading to tighter global supply. Alternatively, other nations may expand production, balancing the market over time.

Short-term effects may include lower US grain prices and higher global prices due to trade disruptions. Long-term shifts in trade patterns could reshape global grain markets, depending on how other producers respond.

UK Market

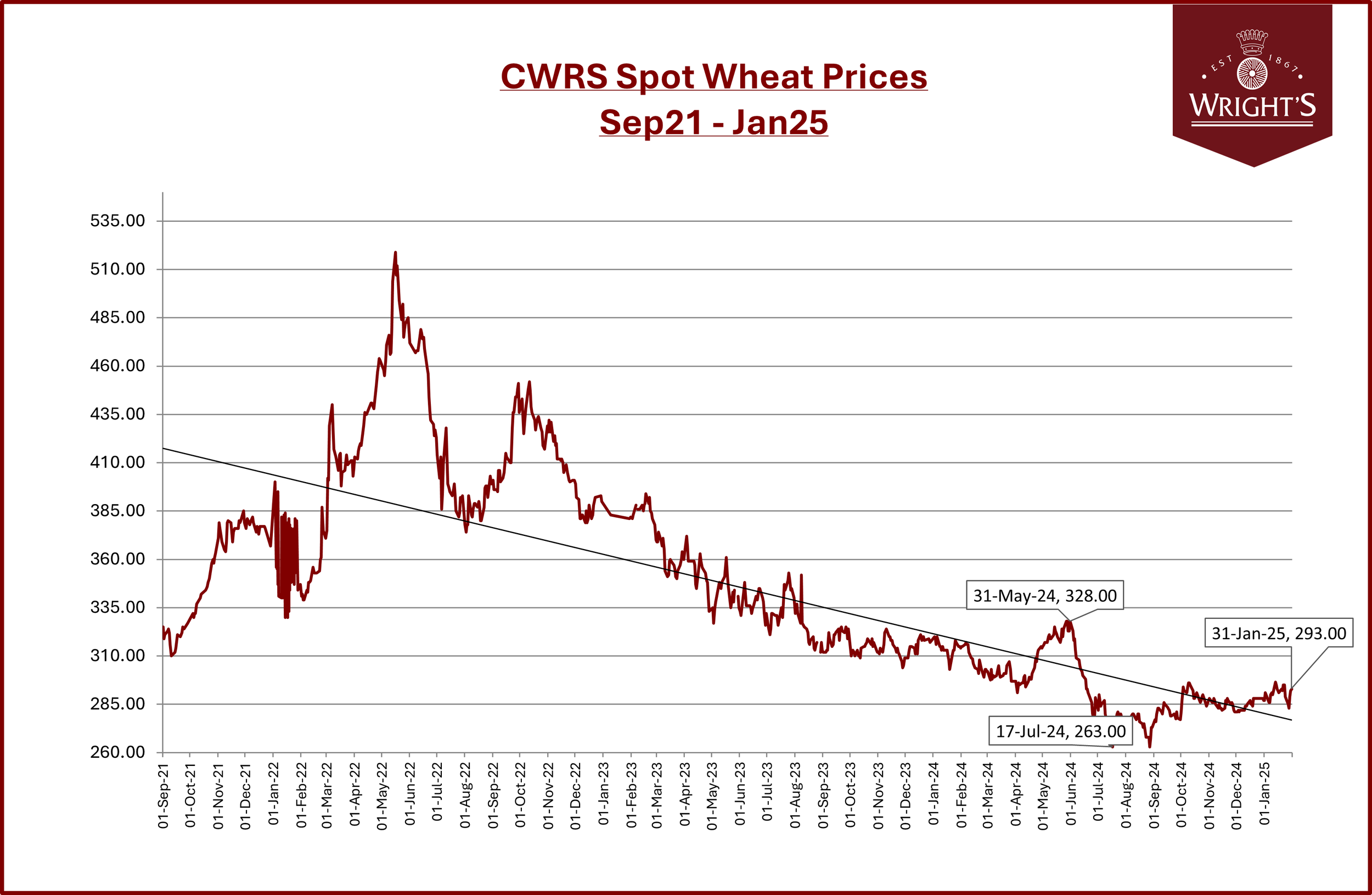

The AHDB published the latest 24/25 UK Supply and Demand estimates for wheat, barley, maize and oats this week. Wheat exports for the full season are expected to reach 175 Kt, marking a 32% decline from last year and the lowest level recorded since at least the early 2000s. So far this season (July–November), exports have amounted to just 51.6 Kt, which is 62% lower than the same period last year. This suggests that export activity may increase in the latter part of the season. Despite a smaller harvest tightening supply, the significantly reduced export volumes mean that wheat stocks are set to be particularly high. By the end of the season, the UK is projected to hold 2.708 Mt of wheat, well above the five-year average of 2.116 Mt. This coupled with lack lustre demand domestically and a continuing inflow on imported wheats keep the market bearish. Milling wheat premiums have remained steady over the last couple of weeks, with imports continuing to keep a lid on any uptick in these figures.